H2 2026 Copper Contracts: Buy Now or Wait?

Every procurement cycle has a decision window. For copper concentrate, that window for H2 2026 supply is open now — and the supply-side signals suggest it will narrow faster than in previous cycles.

Here is a structured look at the timing question: what the “wait” argument assumes, what the “buy now” argument is actually based on, and what a practical decision framework looks like for Japan-based manufacturers and trading companies.

The Setup: Where the Market Stands

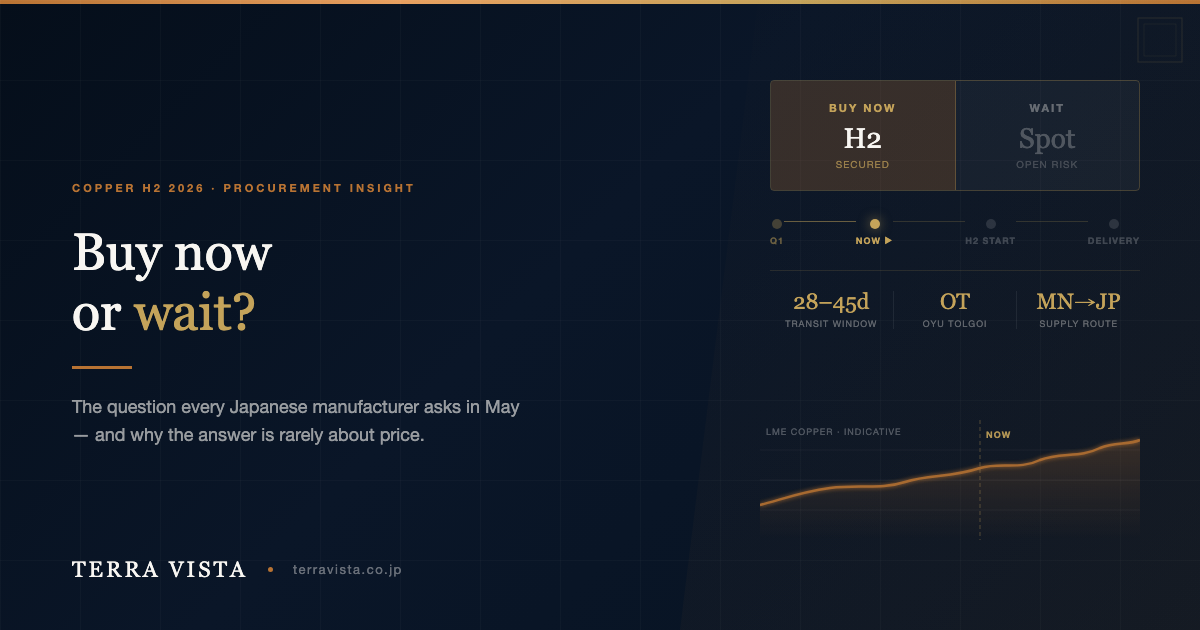

As of Q2 2026, LME copper spot is trading at approximately $10,100/MT — up 8.3% month-on-month and 25% year-on-year.

🟡 LME spot: MetalCharts/MINING.COM, May 2026

Japan’s copper import premium for 2026 was set at a record $330/MT — 3.7 times the 2025 level of $88/MT.

🟢 Source: Pan Pacific Copper benchmark, Mining.com January 2026

These two numbers together tell the same story: Japanese buyers are already paying more for copper, and the competition for reliable supply is intensifying at the upstream level.

The procurement timing question — buy H2 supply now or wait — is not an abstract market call. It is a structural question about how copper concentrate supply chains work and what the realistic alternatives are at different points in the year.

How Copper Concentrate Procurement Actually Works

Unlike refined copper traded at LME, copper concentrate is procured through negotiated supply relationships. The key mechanics:

Annual benchmarks set the TC/RC baseline. Treatment charges (TC) and refining charges (RC) are negotiated annually between major producers and smelters. The 2026 China-Japan benchmark was set at approximately $21–23/MT — near the low end of the historical range.

🟡 TC/RC benchmark: industry consensus figure, Q1 2026 negotiations

Low TC/RC = concentrate is tight. When smelters have abundant feedstock, they charge more for processing (higher TC/RC). When they compete for concentrate supply, they accept lower charges. The current low-TC/RC environment is a direct signal of upstream tightness.

Supply is relationship-allocated before it reaches spot. Producers like Oyu Tolgoi (OT) commit volumes to long-standing buyers in Q1-Q2 for the following contract period. Once committed, that volume is no longer available at spot. Buyers who rely on the spot market in Q3 are purchasing from volumes that were not fully allocated — and those volumes carry risk (specification variability, shorter delivery windows, less predictable documentation).

The practical implication: by the time a buyer in Q3 decides they “waited long enough,” the best-quality, most reliable supply has already been allocated.

The “Wait” Argument — and Its Assumptions

Buyers who choose to wait through Q2 typically make one or more of the following assumptions:

- LME prices will pull back — reducing the effective cost of copper feedstock

- Spot availability will improve — freeing up volume for later negotiation

- Alternative sources will emerge — providing optionality not currently visible

Each of these assumptions deserves scrutiny.

On LME price pullback: Copper prices are being supported by multiple structural drivers simultaneously: Chinese strategic stockpiling, EV and power-grid infrastructure build-out, and the US-Japan Critical Minerals Action Plan (signed March 2026). These are not speculative forces. They are policy-backed demand signals with multi-year lead times. A cyclical pullback is possible; a structural reversal is not in the base case for H2 2026.

On spot availability improving: The OT underground mine ramp-up is adding volume to the market — but that volume is being absorbed by Chinese smelters under existing allocation agreements. New volume entering the spot market depends on producers choosing to sell spot rather than extend existing relationships. There is no structural reason to expect this in 2026.

🟡 OT 2026 production guidance: Rio Tinto Q1 2026 Production Report. Underground ramp ongoing; medium-term production target ~500,000t/year by late 2020s.

On alternative sources: Buyers who are not currently in active negotiation with Mongolian producers — and do not have an intermediary relationship — face a 2-4 month timeline to establish the documentation, counterparty verification, and logistics coordination needed to begin a new supply relationship. Starting that process in Q3 means Q4 at the earliest for actual supply. H2 has already passed by then.

The “Buy Now” Argument — What It Is Actually Based On

Securing H2 2026 supply in Q2 is not a bet on prices moving higher. It is a decision to remove supply-chain risk from the equation.

Specifically:

1. Allocation timing. OT volumes and equivalent Mongolia-origin concentrates are being committed now. The buyers in active negotiation today have first access to supply that matches their specification requirements. Waiting shifts the available pool toward residual volumes.

2. TC/RC leverage. In a tight-concentrate environment, buyers who are negotiating now have more leverage on TC/RC terms than buyers negotiating under time pressure in Q3. This is a cost-efficiency argument, not just a supply-availability one.

3. Documentation and logistics lead time. Mongolia-Japan logistics via the Trans-Mongolian rail corridor run 28–45 days under normal conditions. 🟡 (Operational estimate based on known Trans-Mongolian route parameters.) Factoring in pre-shipment inspection, customs documentation, and Japanese import compliance — the effective lead time from “signed contract” to “delivered concentrate at Japanese port” is typically 60–90 days. H2 delivery starts in July. Working backwards: a contract signed in late May or early June supports July-August delivery. A contract signed in August supports October delivery at earliest.

4. Japan import compliance. Japan’s import regulations for copper concentrate involve a specific set of documentation requirements: certificate of analysis, country of origin declaration, REACH compliance records, and customs clearance through licensed importers. First-time relationships with new suppliers require additional time for compliance review. This is not a blocker — it is a lead-time factor that favors early action.

A Decision Framework

The buy-now-or-wait question ultimately depends on your procurement objectives:

| Objective | Recommended Timing |

|---|---|

| Maximum supply reliability for H2 | Act in Q2 (now) |

| Best TC/RC leverage | Act in Q2 (now) |

| Flexibility to respond to price movement | Act in Q3 (with spot availability risk) |

| Exploring new supplier relationships | Begin process now; delivery in Q4 |

For buyers with existing supply relationships, the decision is mainly about volume extensions and TC/RC renegotiation — that negotiation is already happening.

For buyers without established Mongolia-origin supply relationships, the practical timeline matters: beginning the process in June or July means H2 delivery is unlikely; it positions you for Q4 2026 or H1 2027. That may be the right outcome — but it should be a deliberate decision, not an accidental one from delayed action.

What Terra Vista Does in This Context

Terra Vista Co., Ltd. (テラ・ビスタ株式会社) is a business consulting and market entry advisory. We coordinate copper concentrate procurement from Mongolia-based suppliers for Japanese importers and manufacturers.

We do not hold inventory. Our role is counterparty qualification, documentation coordination, logistics oversight, and Japan compliance support — reducing the time and risk associated with establishing a new Mongolia-origin supply chain.

If you are evaluating copper concentrate procurement for H2 2026 or H1 2027, and want to understand what accessing Mongolian supply looks like in practice, contact us at ranky@terravista.co.jp or visit terravista.co.jp.

Frequently Asked Questions

When is the practical deadline to secure H2 2026 copper concentrate supply from Mongolia?

For shipments arriving in Japan by September 2026, the contract and logistics coordination timeline requires finalizing supplier agreements by late June at the latest. Earlier is better — Q2 negotiations have better supply optionality and TC/RC leverage.

What is the current TC/RC benchmark for Mongolia copper concentrate?

The 2026 China-Japan annual TC/RC benchmark was set at approximately $21–23/MT for copper concentrate. This is at the low end of the historical range, reflecting tight concentrate supply conditions globally.

Why is Japan’s copper import premium so high in 2026?

The 2026 premium of $330/MT (set by Pan Pacific Copper) reflects intensified competition among Japanese buyers for upstream supply, combined with reduced availability from traditional South American sources and rising strategic demand driven by Japan’s critical mineral security policy.

What are the logistics options for Mongolia-to-Japan copper concentrate?

The primary route is via the Trans-Mongolian railway to Chinese ports (Tianjin or Qingdao), followed by sea freight to Japanese ports (Yokohama, Kobe, Nagoya). Transit time is approximately 28–45 days from loading. An overland-only route through Russia exists but is currently subject to logistics disruption risk.

Does Terra Vista hold copper concentrate inventory?

No. Terra Vista is a procurement intermediary. We coordinate supply relationships between Mongolia-based producers and Japanese buyers, handling documentation, logistics oversight, and compliance — we do not hold physical inventory.

Terra Vista Co., Ltd. (テラ・ビスタ株式会社) | business consulting and market entry advisory | Supply chain coordination for mineral procurement, Japan market entry support, and cross-border B2B trade

terravista.co.jp | ranky@terravista.co.jp

Related Terra Vista service: Supply Chain Orchestration → — China and Asia sourcing with certification, MOQ and sample verification built in.

Talk to our team

Get a tailored answer on sourcing, market entry or compliance — free consultation, three languages.